In March 2020, unregulated crypto exchanges, led by Binance, switched to USDT as collateral for margin trading. This has led to a progressive release of around 1 million Bitcoins previously locked as collateral. The fact these newly available Bitcoins didn’t crash the price only makes sense if Tether scooped them up and is now holding them as reserves.

The price of Bitcoin is determined, same as for all assets, at the margin. The price is a market equilibrium between how many Bitcoins are available for trading, and how many Bitcoins are needed for daily flows:

$BTC = Turnover / Supply

This formula is quite straightforward: the price of Bitcoin rises with increasing use cases, and decreases with the amount of Bitcoins competing for these use cases. Note that Supply only means “Bitcoins available for trading” - all the Bitcoins sitting in HODL wallets don’t take part in the price discovery process.

Bitcoin price and turnover

There are three types of Bitcoin turnover:

- short term (a few days), for transfers (capital flight from China, unregulated exchange account funding, remittances)

- medium term (a few months), for collateral and arbitrage (margin trading, Grayscale premium arbitrage)

- long term (a few years), for HODLing

There are also two types of one-way flows, impacting the amount of Bitcoins available:

- lost coins (reducing the Supply, positive for price)

- mining rewards (increasing the Supply, negative for price)

The first three flows compete for the Bitcoins that are available for trading at that time (“S” for Supply). For instance, if Bitcoins were only used for transfers, and people were using Bitcoin to transfer $10 billion per day, assuming an average transaction length of 1 day, the price of Bitcoin would be:

$BTC = $10B / S

If the Supply is 1 million Bitcoins, that would give you a $BTC market equilibrium price of $10,000. The idea is that people who use Bitcoin for real world use cases don’t care about its price, and will simply buy an amount in fiat that they need for their purpose, while the Bitcoins available for trading will compete for that fiat.

All things remaining equal, you have two rules:

- The lower the Supply, the higher Bitcoin’s price, and vice versa

- The higher the flows, the higher Bitcoin’s price, and vice versa

The impact of USDT replacing Bitcoin

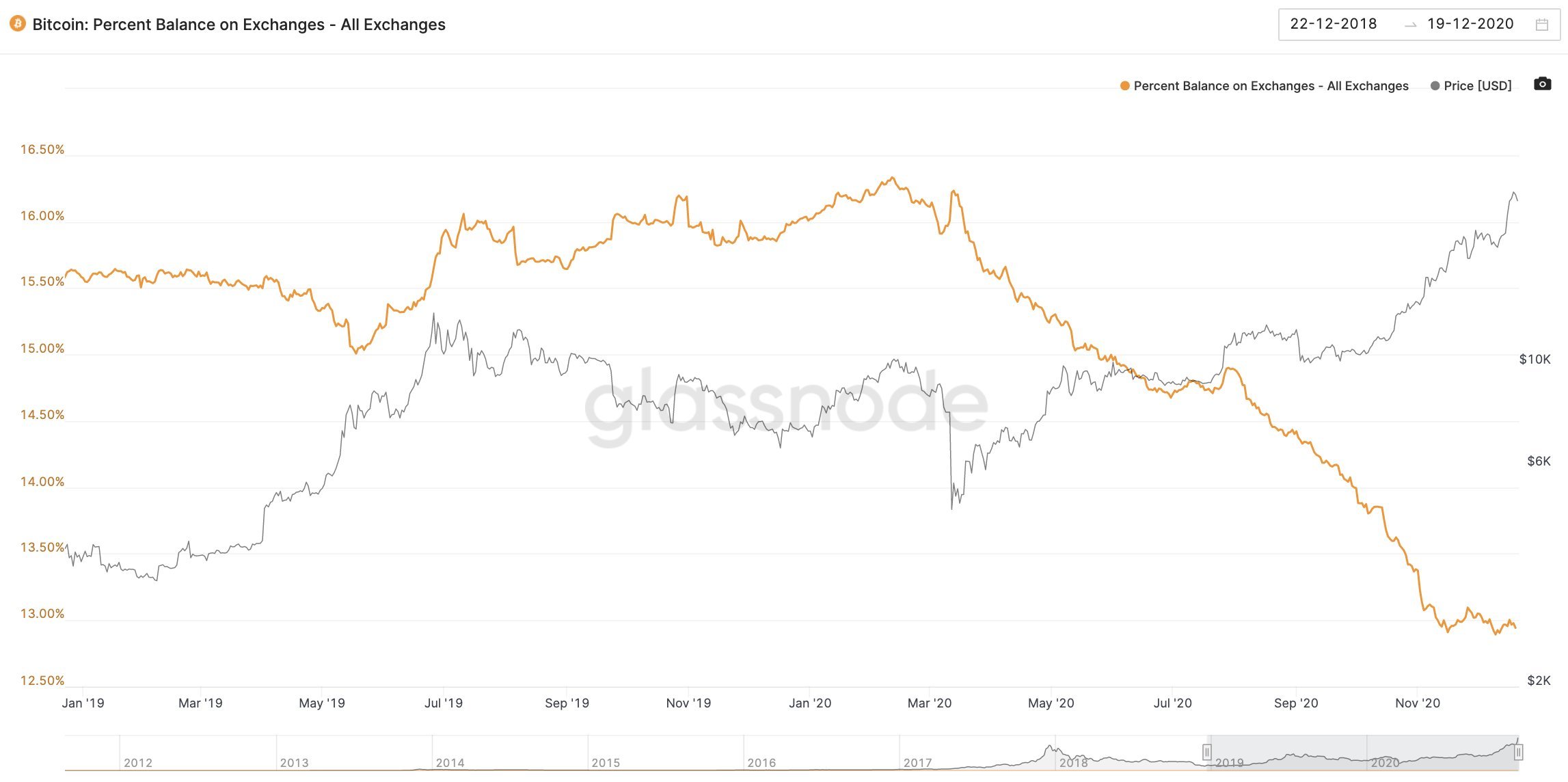

Ever since exchanges started replacing Bitcoin by USDT for margin trading collateral, the amount of Bitcoins at exchange-controlled wallets has steadily decreased:

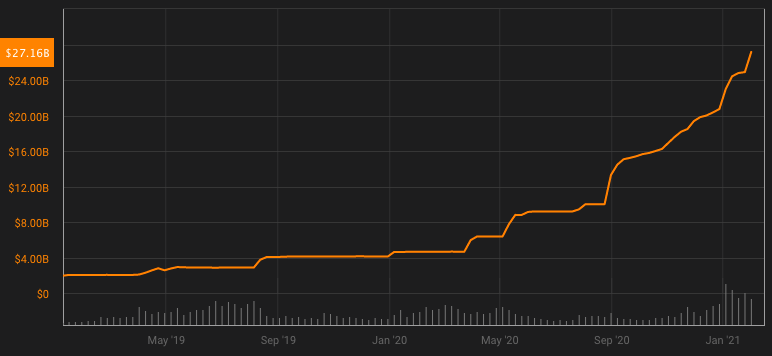

This trend has, of course, been compensated by a relentlessly increasing amount of USDT in circulation, to the tune of Bitcoin outflows multiplied by their price:

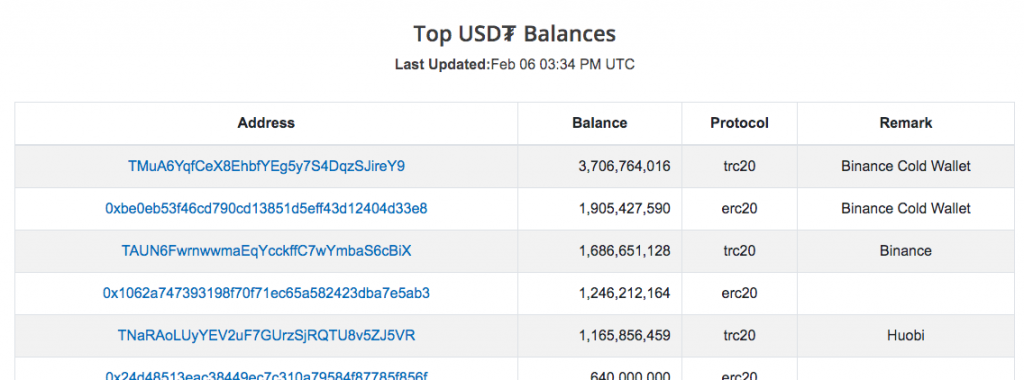

Unsurprisingly, most of these new USDTs sit on exchanges, Binance being on the top of the list, as they’re being used as collateral:

This move has greatly increased the Bitcoin supply, to the tune of 1 million Bitcoins. These are Bitcoins that have been gradually released from being frozen as collateral, and are now available for other types of use.

The increased acceptance of USDT are also replacing Bitcoin for the transfer use case, as they aren’t volatile, and can be sent almost instantly. This has reduced Bitcoin turnover.

Bitcoin to the moon… HOW?

Given the rise of USDT in circulation has increased Bitcoin supply and reduced its turnover, the impact of the Tether collateral flippening on $BTC should have been disastrous. Yet, Bitcoin is up tenfold since the start of the trend. How is this possible?

The knee-jerk response from Bitcoiners will be that a lot of new demand for Bitcoin has emerged at the same time, citing Michael Saylor’s MicroStrategy and Grayscale. But we’re talking about 1.3 million Bitcoins (released from collateral and newly mined) in less than a year! That’s one hell of an exogenous event that should have crushed the price, right?

Well, no - because the event wasn’t exogenous; it was decided by the crypto community insiders - mostly Binance, Bitfinex and Tether. They knew that by releasing all this Bitcoin into the market, they would crush the price. So, they didn’t.

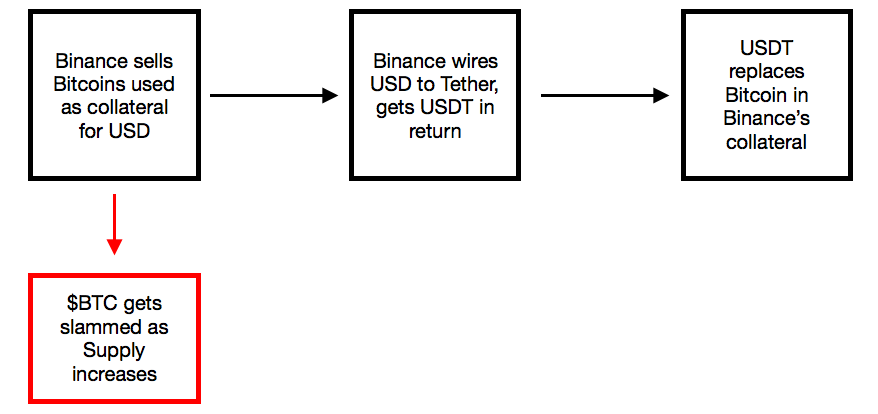

If you were to follow Tether’s own advertised rules, where new USDTs are issued only against matching USD deposits, the Tether collateral flippening should have followed this path:

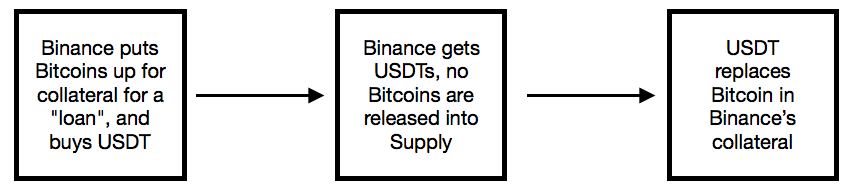

Instead, what happened is this:

This path has two huge advantages:

- no fiat is needed

- no Bitcoins are released into Supply

It also has one small disadvantage:

- Tether has to lie about how USDTs are issued and what its reserves are made of

Note that this disadvantage can be easily solved by round-tripping, a practice that was once dear to Wirecard, where a very small amount of fiat circulates a lot of times between everyone involved, to make it look like there are transactions. Meaning that Binance doesn’t send Bitcoins in exchange of USDT directly to Tether. They first put these Bitcoins as collateral for a loan from Tether, then wire the proceeds of the loan to Tether, and get USDTs in return. Exactly the same result as buying Bitcoin with USDT, but very different appearances and paper trail.

USDTs are backed by Bitcoin

More accurately, Tether’s reserves are loans to exchanges, collateralized by Bitcoin. The Bitcoins that were used as collateral for margin trading, are now used as collateral for USDT. This way, exchanges know that USDTs are actually worth something, and accept to maintain the 1:1 peg. And no fiat needs to be deposited at Tether, a small and shady company with no offices, under investigation by the NYAG, with a shaky banking relationship with Deltec that’s not even a real bank.

This is the only way the Tether collateral flippening wouldn’t have crushed Bitcoin’s price. The question that remains to be answered is, if exchanges accept that Tether issues USDTs backed by Bitcoin, why not print some USDT out of thin air to buy Bitcoin with it, and pump $BTC in an effort to ignite another round of FOMO?