Tether is the entity that issues and manages the USDT stablecoin. The “entity” wording is key: although Tether is incorporated as a Hong Kong company, its offices don’t seem to exist at the filing address, its CEO and CFO are M.I.A., and the bulk of communication is performed by its CTO, Paolo Ardoino.

USDTs are crucially important to the crypto ecosystem. Pegged 1:1 to the US dollar, they enable instantaneous transfers of huge sums of money between industry players, without having to explain to a bank what you’re doing. USDTs are, for all practical purposes, almost like money.

Until they aren’t.

Golden Key Ltd.

In the history of things that are “almost like money”, allow me to introduce asset backed securities (ABS). In the 2000s real estate boom, those were particularly popular, because they allowed to create fiat money without having to comply with banking regulations.

Imagine that it’s 2006, you work at a US-based bank, and you want to give a mortgage to Tom. Tom has no job, no assets, and a passion for face tattoos, but he really wants to buy that condo in downtown Philly, and you really want to give him a mortgage because then you’ll collect your fee. If you were a traditional banker, you wouldn’t give Tom a mortgage because then this mortgage would sit on your balance sheet and burn a hole in it when Tom’s new condo goes up in flames because cooking meth is dangerous. But if you’re a modern, 21st century banker, you know that you don’t have to keep that mortgage on your books. You can securitize it - bundle it together with a bunch of other mortgages, and post this bundle as collateral for a whole new security, which investors from Dusseldorf, Germany will buy at face value because they think they’re sophisticated and must invest in sophisticated things.

That’s how ABSs came into existence - new securities, fully backed by assets (hence the “A” and “B” in the name), that you could structure to look like anything - 30 year bonds, or money market instruments. They had cool sounding names, too. Like Golden Key.

Asset Backed Commercial Paper

Commercial Paper is a short term bond (less than 365 days in maturity) issued by a commercial entity - a bank, a governmental institution, a corporation like Coca Cola. They are the bread and butter of money market funds, because you are allowed to price them linearly when their maturity is less than 90 days, making your fund’s performance look very smooth.

Asset Backed Commercial Paper (ABCP), on the other hand, is issued by a Special Purpose Vehicle (SPV), a shell company with no real activity. Because nobody would lend money to a shell company with no real activity, its commercial paper is backed by assets (“A” and “B” again). The SPV is regularly audited, and investors are confident that the SPV is properly collateralised, and lend it money by buying its ABCP. The full beauty of it, is that by funding your SPV in the money markets, taking out short term loans, while backing it with long term, illiquid assets, you keep the liquidity and term premiums for yourself, without pesky banking regulators knocking on your door. The SPVs look like banks, but aren’t. That’s why they quickly became known as part of “shadow banking”.

SPVs were usually managed by real banks, because banks know how to do all this structurisation and hedging and commercial paper issuance and marketing and rating stuff. Golden Key, for instance, was managed by Barclays. And it had a stellar P-1 rating, which is the “AAA” equivalent for commercial paper. This P-1 rating made it eligible for the largest and well-known money market funds, and those funds bought Golden Key ABCPs hand over fist, funding its underlying portfolio of assets.

Barclays was acting as a broker for Golden Key, meaning that it was responsible for buying assets on the market and sell it to the SPV, so that the SPV had assets to back its ABCP.

Almost like money

For a couple of years, Golden Key acted like a savings account, paying good interest. Not stellar interest, because it was very low risk, but fair interest nonetheless - something like 3 month Euribor plus 3-4 basis points. Which, for a P-1 rated ABCP, was a good margin at the time. Not a stellar margin, but a fair margin nonetheless. Money market fund managers would roll it every three months, meaning that they would reinvest money into the same ABCP as it came due.

It was such a dull, boring job that money market fund managers usually left their jobs before noon to get lunch and wouldn’t check back in until the next morning. Come in at 8 a.m., roll the commercial paper that’s coming due in two days before 9 a.m., and then bore yourself to death, day after day.

It was so widely accepted that these ABCPs were dull boring things, that the day when Golden Key suddenly blew up, nobody could even find the prospectus for the ABCP (meaning the set of documents that describe how it works, and what kind of assets back it). It took hours of frantic calls to brokers and lawyers in the Cayman Islands to get these hundred-page-long legalese page-turners.

Fiduciary duty? lol

For years, i.e. for as long as money market fund managers were reinvesting their fund into the same ABCP and nobody needed to cash out, Golden Key acted like a saving account. But, the moment the first market tremors of the 2007 ABS crash began to rumble, Golden Key went bust.

You remember how Barclays was supposed to act as broker for Golden Key, meaning that it would buy something on the market, and sell it to the SPV at the same price? Well, Barclays did just that - but not on the same day. It wasn’t explicitly written in the ABCP prospectus that both legs of the trade needed to be performed within a certain time period. So, when markets began to go south, Barclays went through its books, and sold to Golden Key the worst of their crap, at prices it had bought that crap months ago - basically, at par. Good-bye losses, hello year-end bonus!

And they got away with it. Why wouldn’t they? Caveat emptor, suckers! Money market fund managers had assumed that something was safe and sound because it looked that way for a long time, and because it was convenient for them. And they got caught with their pants down.

Tether

What you need to understand in the case of Golden Key, is that it all looked so very legit. The ABCP had a stellar credit rating from Moody’s. It was managed by Barclays. Its accounts were audited. It was traded by the largest money market funds in the world. It was governed by hundreds of pages of legalese. You could see it on your Bloomberg terminal. It was so, so very legit and backed by assets and worth 100% until it wasn’t. Billions of dollars that you thought were yours, became somebody else’s.

Fast forward thirteen years, and now you have Tether and USDT. 22 billion almost dollars governed by a five-page disclaimer that USDTs are backed by whatever Tether wants, at whatever valuations Tether finds convenient. No credit rating, no bank, no auditor, no offices, no CEO and CFO, no guarantee whatsoever.

Backed by reserves

The whole angle of attack of Tether sceptics is that USDTs aren’t backed by US dollars. This would mean that Tether can print USDTs out of thin air, for as long as USDT bagholders believe that their coins are legit, and don’t try to sell.

Tether, and most of the crypto community, contest that claim, or at least try to deflect it. USDTs are very convenient, because they allow everyone to bypass banks and their AML and KYC regulations. You know, very much like ABSs allowed to bypass capital requirement regulations. And USDTs have looked like real money for such a long time, why not assume that they will continue to look like money in the future, too?

Rug pull, sucker

I don’t believe that USDTs are backed, but I also don’t know that they’re not. So let’s play devil’s advocate and assume that there are indeed 22 billion of real US dollars hidden somewhere in bank accounts, controlled by Tether.

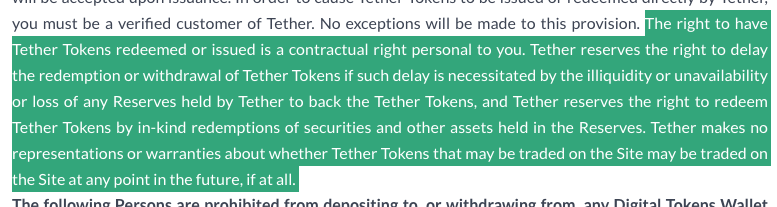

When people try to cash out en masse, i.e. redeem their USDTs for real money, why would Tether allow them to do so? 22 billion dollars is a lot of real money. Why give it up? Tether’s own website says they don’t have to. Seriously, I’m not making this up:

Why should Tether spend all its money (it is theirs, after all - USDT holders don’t have a legal claim on Tether’s reserves) trying to save the crypto markets, when they collapse? How many years would it take them to rebuild their war chest, assuming that crypto bounces back? Paolo Ardoino will be old and sick by then. Why not party on a yacht in Monaco for the rest of his life instead?

If USDTs become worthless, it’s the end of the crypto ecosystem. A lot of Bitcoin investors have USDTs in their portfolios, too. If Tether collapses, and redemption requests hit, they’ll have to sell whatever they can. Except there won’t be any exchanges left, for most can’t function without USDTs, and the rest (like Coinbase) will crumble under the tsunami of requests, and there won’t be any bids left. Other stablecoins will collapse, too, as holders rush for the exits.

Caveat emptor.

Thanks for another great post. Tether is now “worth” 22 billions, which only is something like 2% of the total crypto market. Will it matter if it goes bust? I have a feeling hardcore crypto maniacs will shrug and just buy the dip that comes with the bust.