Since crypto’s near-death experience of March 2020, three things have risen in tandem: the price of Bitcoin, the market cap of Tether, and the number of people under lockdown at home, turning to day-trading as a way to kill time. These three trends are closely intertwined.

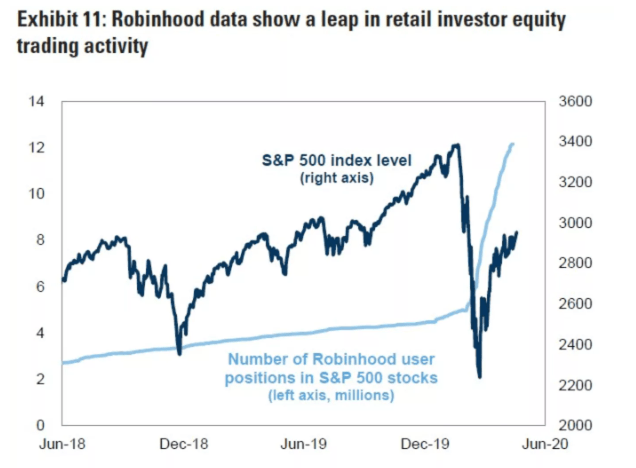

An image is worth a thousand words, so just have a look at this chart of Robinhood users’ activity:

A combination of high markets’ volatility, stimulus checks, and having nothing better to do, has led millions of people to start trading - or gambling, depending on your opinion on the financial markets.

Robinhood is one way to have fun, betting on stocks. But there’s another, much more adrenaline-fuelled alternative: crypto. The keyword is leverage. Stock trading apps will allow you to lever your trades 3, 4 or 5 times, depending on their assessment of market volatility and the risk of not being able to close your position in time. Unregulated crypto exchanges like Binance will offer you up to 125x leverage. Now that’s gambling on steroïds.

This leverage is the lifeblood of the crypto economy. To understand how it works, allow me to entertain you with a short story.

Online Forex trading and leverage

A long time ago, BNP Paribas bought a retail forex exchange, because they thought they’d get an insight into forex trading flows and positions. What they quickly discovered, is that the website was a muppet slaughterhouse.

People would get stopped out ALL THE TIME because they used too much leverage. Over 90% of them lost money in a consistent way. Those are worse than even casino odds. That’s why around 2005, you had so many forex trading websites popping up. They would offer up to 500x leverage. Anyone using that leverage would get wiped out in minutes by random moves. The trading websites wouldn’t even hedge their overall positions - the certainty of loss was that great. Because of this, the business was extremely lucrative.

The higher the leverage, the better (for the website). This became such a huge trend that regulators stepped in, and introduced maximum leverage rules. Something like x30 for forex, if I remember correctly. All of a sudden, all the ads and Premier League sponsorships vanished.

Forex gambling is still around, but not nearly as profitable, because it takes time for people to lose their money with a pitiful x30 leverage. Currencies usually don’t move by 3% in a day. It can take weeks for an amateur trader to lose it all. Plus the adrenaline rush is gone.

Crypto trading and illegal leverage

Enter crypto. It’s hard to overstate how one-sided leveraged crypto trading is. Traders don’t stand a chance. With currencies, you could expect to extract SOME money from real world flows. In crypto, there are no real world flows. It’s just traders against traders against insiders.

Of course leveraged trading is very fun and addictive. So the flows are substantial. Regulated exchanges don’t offer leverage, because it’s a pain in the ass legally - just look at Coinbase dropping it recently. Because cryptos aren’t currencies, you have to deal with all this crap about ownership and being able to deliver the goods that’s very hard to process. Plus the CFTC thinks cryptos are commodities, while the SEC thinks they’re securities, and you have to deal with regulations for both.

That’s why offshore, unregulated exchanges sprung up so fast to offer leveraged crypto trading while bypassing those pesky regulators. Being unregulated offshore operations, it’s very hard for them to establish and maintain banking relationships, so they rely on cryptocurrencies, mainly Bitcoin, as a means for their clients to top up their accounts. If you’re a US resident, you can’t deposit money on Binance using your credit card. Instead, you go on Coinbase, buy Bitcoin, and send it to Binance.

Those exchanges are an absolute bonanza, precisely because they create this huge demand for crypto for on-ramp purposes. This crypto is then lost by gamblers, thanks to insane leverage, back to the crypto industry. This creates a one-way flow of real cash into the system.

Of course, these unregulated exchanges are also a huge threat to the crypto industry, because they’re serving US residents, which is illegal, and regulated exchanges knowingly serve as on-ramp platforms and enable US citizens to fund their gambling accounts there. It all hangs on a very thin thread.

Illegal gambling: the real source of revenue for crypto

Offering people to buy Bitcoins to hold isn’t nearly as interesting a business as offering people to buy Bitcoins to fund their gambling addiciton, and lose them by getting stopped out on Binance. A HODLer is a risk because he can sell his Bitcoins. A rekt gambler will simply buy more.

Unregulated offshore exchanges are feeding the rest of the crypto industry. They’re also feeding regulated exchanges, who serve as on-ramp platforms. It has become such a huge business that, just like with forex, regulators are looking into it. The story of Arthur Hayes, the billionaire cofounder of BitMex currently hiding from prosecutors in New York, is one example of authorities breathing down the neck of these underground casinos posturing as exchanges.

These exchanges couldn’t exist without crypto - not least because there wouldn’t be anything to trade, but also because they couldn’t accept customer deposits or meet redemption requests. Were they to rely on traditional banking relationships, a regulator would simply need to call their bank, and order them to shut down their account (just like what happened to Bitfinex with HSBC).

But thanks to this multi-layered system where regulated entities (like Coinbase) allow people to buy Bitcoin, and then help them to send this Bitcoin to less-regulated and/or unregulated entities like BitMex or Binance, everyone benefits. This way of doing things goes back to 2013, when the FinCEN ruled that crypto exchanges are money transmitters, which was an incredibly generous classification, as it absolved the exchanges from performing AML and KYC on crypto transactions.

This very classification is currently under attack from regulators now, with the STABLE Act, and calls for regulating self-hosted wallets. It’s probably the reason why PayPal chose not to allow people to withdraw their crypto.

March 2020: the day when Tether got its wings

While gambling addicts might not care about having to go through Bitcoin to fund their accounts, exchanges themselves would be in a tough spot if they had to rely exclusively on this volatile and cumbersome cryptocurrency to manage your day-to-day operations. Imagine having your liabilities fixed in USD, when your income and assets fluctuate in value by 10% every few hours.

It’s much more convenient to have something that’s stable in price, and can be transferred in seconds. This is where Tether steps in, by offering their stablecoin, USDT. (more precisely, they stepped in gradually, because them relying on the OMNI layer, which itself relies on Bitcoin, made transactions slow and unreliable in moments when the Bitcoin network became clogged - an issue that was solved by launching an ERC-20 USDT token in September 2017).

USDT does have one major flaw, however - it’s controlled by a central party, Tether. By holding USDT, you are accepting Tether’s credit risk, which is a scary thought, knowing that they aren’t audited or regulated, and are currently under investigation by the NYAG. USDT tokens can be frozen, and there’s no guarantee that you’ll be able to cash out. It’s probably for these reasons that USDT usage remained subdued for quite a while.

But then, something happened. Unbeknownst to most, March 2020 was a crucial turning point for the crypto ecosystem.

8. The recent rapid increase in USDT issuance since March and then since Oct are entirely explained by (1) post 03/20 there was a sustained mass move away from BitMEX (which margins their deriv contracts in BTC) towards Binance (which margins mostly in USDT)…

— David Fauchier (@dfauchier) January 17, 2021

For some reason, major unregulated exchanges suddenly warmed up to the idea of holding a lot of USDT on their books. The switch from Bitcoin as collateral, to USDT for margin trading, meant that Binance was cool with having a multi-billion dollar exposure to Tether, a small unaudited company with no office, whose CEO and CFO are MIA.

Only insiders know the true reasons behind this shift, but my take is quite straightforward:

- with Bitcoin in freefall, major institutions in the crypto industry had to come together to support the markets - much like commercial banks bailed out LTCM in 1998 to prevent a financial panic

- having Bitcoin as collateral for margin trading is a nightmare for risk management (because the value of the collateral is correlated with the P&L of the trade), and exchanges needed something stable to prevent a meltdown of cascading liquidations

Follow the Tethers

Given the explosion of online trading due to the lockdown, it’s not hard to imagine how the demand for USDT skyrocketed, as exchanges needed to fund their client’s margin positions. The increase of USDT would then mirror, to an extent, the inflows of money in the crypto gambling ecosystem.

At the same time, this explosion of trading activity meant big profits for the unregulated exchanges, which propped up Bitcoin as those exchanges stored at least a portion of their gains in Bitcoin. Remember that their activity being on the very edge of the law, having all of their assets sitting at a bank wouldn’t be the smartest move.

But here’s the heart of the Tether controversy. According to Tether, new USDTs are issued only against equal deposits of USD. Why would unregulated exchanges, in a sudden change of heart, accept to bear unlimited Tether credit risk? To have your money stashed in Tether’s bank account is much worse than to have your money stashed at your own bank account. USDTs are not legal claims on Tether’s reserves. Why would Binance hand over $7 billion in exchange of very practical, but legally worthless database entries?

Again, looking at traditional finance, the “USD deposit” story is bullshit. Banks don’t send each other dollars. They sign IOUs. It’s much more practical. And, were exchanges and Tether to use the same practice, it would mean that Tether issues USDTs - its own IOUs - against IOUs from exchanges. This greatly reduces credit risk, as instead of having $7 billion of their money sitting in Tether’s bank account, Binance could simply acknowledge that they owe Tether $7 billion - assuming, for example, that their own 7 billion USDTs aren’t frozen or otherwise not usable.

The problem of such an arrangement is, of course, that Binance could just borrow USDTs from Tether (which would print them out of thin air), and do whatever they want with them - manipulate markets, buy Bitcoins for their own account, you name it.

And it’s for this reason that Tether’s refusal to perform an audit, or simply to state what exactly their “reserves” are, is very, very suspicious.

Bitcoin’s “store of value” status

Correlation isn’t causation, but a lot of people like to think that the growth of Tethers is proof that the “Bitcoin economy” is flourishing.

What explains the correlation between Tether issuance & bitcoin’s price? One theory is that Tether causes bitcoin. I think it’s more likely that bitcoin causes Tether. A rising bitcoin price means a bigger bitcoin economy, and so more Tethers have to be drawn-out to support it.

— John Paul Koning (@jp_koning) November 25, 2020

But what is this “Bitcoin economy”, exactly? Illegal gambling by people who are under lockdown with nothing else to do, funded by a shady corporation under investigation by the NYAG, and under the imminent threat of new legislation?

In this equation, Bitcoin looks much less like “digital gold”, than equity in an underground casino run by the mob. The last year was good, as a lot of people turned up to gamble their stimulus checks away. But when the tide turns, do you really think the mob will allow you to cash out?

The clock is ticking. The lockdowns will end. The NYAG will announce its findings soon. Regulators will clamp down on stablecoins. And during all this time, miners are burning $20 million per day just to keep the Bitcoin network up and running.

Edit: as I was writing this post, John Paul Koning tweeted this. I guess there’s a sense of agreement in the air.

Western nations have mature, liberalized gambling sectors. Nations like Nigeria & Brazil do not. Which may explain why cryptocurrencies are so popular there: they fill a void left by the absence of casinos, online poker, sports betting, etc.

— John Paul Koning (@jp_koning) February 6, 2021

Chart via https://t.co/FuFKv9y8q0 pic.twitter.com/S2uAU2221b