Tether has become a plain old fiat central bank, issuing new USDTs against debt. USDTs are backed, but not by US dollars. They are backed by promises to make good on their debts by the receivers of newly minted USDTs.

While it’s not fraudulent per se, the fact that USDTs aren’t backed by US dollars opens the door to unlimited USDT printing. The gatekeepers are the people in charge of the Tether printing press. In an ideal world, they should ensure that proper reserve requirements are met and that the receivers of newly minted USDTs are properly capitalised.

However, Bitcoin’s exponential price rise, happening in lockstep with ever-increasing USDT issuance, shows that the Tether press has gone in overdrive. When the mania will end, crypto investors will lose everything, in a second.

The Tetheral Reserve

Long gone are the days when Tether claimed that USDTs were backed by cash. Its own website states:

It’s not necessarily a bad thing for the crypto ecosystem that Tether doesn’t have cash on hand to the amount of USDTs issued. First off, that would be a central point of failure. Tether the institution is currently under investigation, USDTs are used for money laundering, and having $20 billion in a bank account would expose you to having your assets frozen - as has already happened in the past.

It’s much more practical to have all your assets in loans to counterparties, from a solvency and operational point of view. The problem is, of course, that is exposes you to:

Liquidity risk

The role of USDTs is to replace US dollars in the crypto ecosystem. USDTs are much easier to transfer, because you don’t have to deal with a bank that will ask you all sorts of questions about the origins of the funds, the purpose of the transfer, and the identity of the receiver. In short, you don’t have to bother with AML (“anti money laundering”), KYC (“know your client”), and capital controls regulations. In shorter, USDTs empower you to launder money.

But as much as USDTs are more practical than US dollars, their usage requires convertibility. We live in the real world where nobody accepts USDTs as payment, and you need to be able to cash out your USDTs for real money. You can do this by buying Bitcoin with USDTs on an exchange that trades the BTC/USDT pair, wiring them to an exchange that trades the BTC/USD pair, and cash out. Or, if you are a big player, you can go to a crypto OTC desk and sell your USDTs directly for cash:

This act of financial hot potato, where someone else buys your USDTs, works for as long as the crypto bull run goes on. However, you need a backstop for when things go south, namely, when people suddenly stop wanting to acquire USDTs, and want to cash out for real money. Then, someone has to redeem the USDTs for cash, and that someone should be the issuer: Tether.

If Tether doesn’t have enough cash on hand to process redemption requests, you have a good old liquidity crunch, when panic sets in, and people start dumping their USDT holdings en masse, for whatever price of thing they can get in exchange. Much like a real world financial crisis.

USDT redemptions?

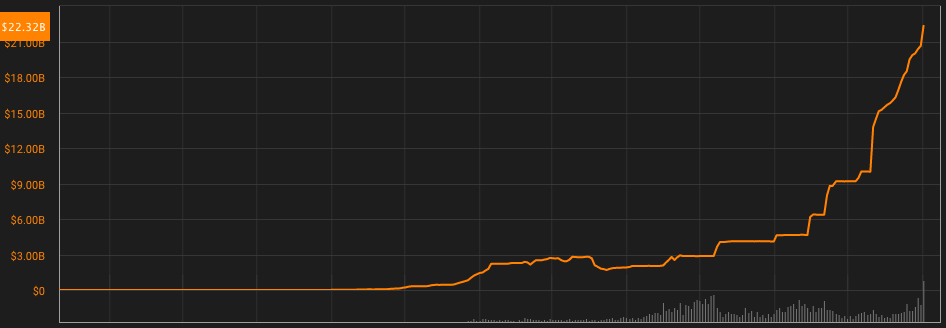

Tether’s willingness to redeem USDTs for real money has been questioned over the last few years, not least because it seems that they’ve ever barely done it, as the number of USDTs outstanding never goes down:

Note that the dip in October 2018 was due to Tether loaning $850m to Bitfinex, not actual redemptions.

Other reasons to question Tether’s willingness to redeem USDTs are the fact that, well, a lot of people couldn’t get Tether to redeem them, despite Tether’s own assurances that proper mechanisms were in place. Moreover, Tether’s own handling of this “FUD” has been anecdotal and shady:

BAM! United against #tether FUD!@rsalame7926 provides proof of redemption as part of one of the biggest players in the industry and @dzrgreg confirms as part of the bank that provides custody and settlement.

— Paolo Ardoino (@paoloardoino) January 4, 2021

YOU GUYS ROCK! https://t.co/sdW171gspT

In the tweet above, the CTO of Tether shares “proof” that USDTs can be redeemed. However, the “proof” is just a list of USDT transactions to and from Bitfinex supposedly performed by an OTC desk, and without a matching set of USD transactions, it means nothing. The original question was, after all:

If anyone…anywhere….has redeemed USDT for USD and can show proof of this transaction I would be happy to compensate you for your time and effort. Thanks! https://t.co/wScl7s1ZAc

— Santiago Capital (@SantiagoAuFund) January 4, 2021

Notice the “redeem for USD” part that gets ignored by Tether. Yup.

The mother of all speculative manias

Remember the real estate bubble of 2003-2007? How people who could barely pay their bills would buy five condos, see their price go up as other people would also buy five condos, and everyone would seemingly get rich out of thin air, together? The reasons for that bubble, in short, were lax lending requirements. A more complete explanation was that banks found ways (thanks to securitisation, reverse engineering credit rating agency rulebooks, and shadow banking) to issue mortgages to people who should have never, ever, qualified for those mortgages. As more mortgages were issued, housing prices went up, in a seemingly infinite loop.

Infinite money

Fiat money is issued against debt. I come into a bank, ask for $10,000, and the bank gives me the money in exchange of me acknowledging that I owe the bank $10,000 - plus interest.

Why can’t I come into a bank and ask for $10,000,000,000? Because banks have rules governing how much they can lend and to whom. The first rule is common sense: if customers aren’t able to repay their loans, the bank will go bust, and because the bank doesn’t want to go bust, it will only lend to people whom it deems creditworthy.

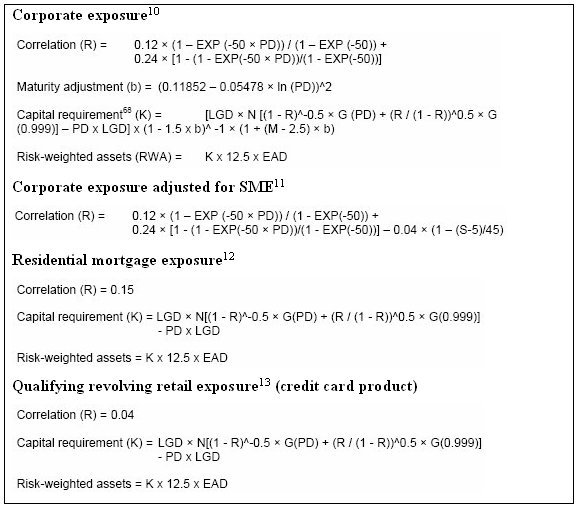

Other rules are regulatory. Banks must have adequate capital to absorb losses on their loan portfolio. It means that their assets must exceed their loans, and the riskier the loans, the larger that excess must be. Banks must also perform maturity matching - meaning that their sources of funding can’t be all short term, when they’re underwriting 30 year mortgages. Then there is risk weighting of assets, Basel II capital frameworks, etc., etc. Just look at this monstruosity:

There are many, many, many rules in place that are intended to prevent bubbles and manias. Despite the meme that “banks print fiat out of thin air”, they don’t - because of those rules. If they did, you’d have a new tulip bulb mania on every Thursday, and civilisation would collapse before summer.

Infinite almost-money

What rules are in place at Tether? What prevents them from printing USDTs out of thin air, without any rules? What prevents Binance from calling Tether and asking for 10,000,000,000 USDTs?

At first glance, the answer is: reality. Were Tether to issue too many USDTs, and start buying BTC and ETH and XRP with it, the price of USDT would get below $1. This has happened in the past, albeit for short periods of time.

But the USDT peg has remained exceptionally stable throughout 2020, despite the greatest financial and economic crisis in recent memory. Exchanges are maintaining the USDT peg, because their very existence depends on it. And USDT has replaced USD in the crypto ecosystem, they cannot allow it to fail. They have USDT on their books. More importantly, their clients own USDT, and account for it as if it were real US dollars. Should USDT’s price fall, people would sell other cryptocurrencies as well, because they’d need to make up for the lost USDT liquidity - and the whole crypto ecosystem would collapse.

Remember, there is a very real need for USDTs, as long as they are pegged to the US dollar, and can be used for immediate, KYC and AML - free transactions.

The USDT/USD peg is founded on the premise that people won’t try to cash out en masse. As long as they don’t, USDT printing can continue.

Creating value out of thin air

Bitcoin doesn’t have intrinsic value. Seriously, it doesn’t. It has no use case (transactions don’t create sustainable demand - you buy Bitcoin, transact, and the other party sells it, a few minutes later), produces no cash flows, gives you no rights or claims. It’s always been a confidence game.

How do you create confidence?

If the higher demand is self-sustaining without manipulation then the manipulation actually bootstrapped genuine value. Maybe like an entrepreneur who aggressively exaggerates the state of development of a project and raises funds but then creates the product and justifies value

— Ari Paul ⛓️ (@AriDavidPaul) February 20, 2018

As long as things go up, and people don’t see any reason why they should stop, things will continue going up. Of course, people at large are unreliable, and they could stop thinking that things will continue going up, because there’s a huge economic crisis, for example. Then things go down very fast:

Had this selling been allowed to continue, there wouldn’t be a crypto ecosystem left to speak of, today. This is why Tether and the exchanges came together and crossed the Rubicon, and decided to create USDT liquidity to stop the selling, by minting a huge 1.6 BILLION USDTs on March 31, 2020, and distributing it across main exchanges.

And it worked. The Tetheral Reserve was born - an infinite pool of USDT liquidity, backed by the exchanges themselves, who committed to hold the USDT/USD peg, in order to save the crypto ecosystem.

To infinity, and beyond

Since that fateful day nine months ago, the Tether press has been picking up speed. As the price of Bitcoin increases, the confidence in the crypto ecosystem rises to new highs, and people don’t bother to question the exponential rise of USDTs outstanding. First of, because the mainstream media doesn’t talk about it - only about the rise of Bitcoin’s price. Then, because insiders themselves start to believe that everything’s fine, and that risks are contained.

I don’t blame them. We’ve seen this sort of misplaced confidence many times over, in the past:

The problem is, of course, that Tether can only print USDTs, and USDTs aren’t US dollars. So when the speculative bubble pops, there won’t be a central bank stepping in to save the crypto markets with real money. The moment people realise that all crypto prices are quoted in USDTs, not US dollars, and that USDTs can only be converted into US dollars when you don’t need it, the music will stop in a second.

Prepare to get filthy rich! In USDT terms.

When you say the traditional banks’ “assets must exceed their loans”, is that different from fractional reserve banking?

I was under the understanding that traditional banks employed fractional reserve banking in which loans may exceed assets by a fixed multiple.

It is different. Fractional reserve banking means that you must have a percentage of all deposits in cash or equivalents. A bank can be bankrupt yet abide by this rule.

Assets must exceed loans because that’s the definition of solvency. You get an idea of a bank’s financial health by measuring how much assets exceed loans. Of course, valuing assets can be tricky, but that’s another story.