Tether’s days are counted - whether by natural implosion, or as a result of regulatory action, the stablecoin funding a wide array of offshore crypto activity will go the way of the dodo.

As is customary in the world of crypto, retail holders will pick up the tab. Offshore traders and DeFi yield farmers will get wiped out. Regulated exchanges won’t collapse overnight, but they will suffer from lost business as people stop buying Bitcoin as an on-ramp for offshore activity, and also from retaliation from regulators.

USDT lifecycle

Tether’s stablecoin USDT is mainly used as a tool for offshore funding. The proceeds of each USDT print are sent mostly to offshore exchanges:

USDTs are mostly used as collateral for margin trading, and for stacking (or “yield farming”). Yield farming is far less reliant on USDT, but it’s still advertised as one of the ways to get eye-watering returns without price risk. With advertised “expected returns” ranging anywhere from 10% to 50%, it happens almost exclusively on unregulated platforms, and the source of returns is… unclear to say the very least. In the real world, anything beyond a 5% ARR reeks of horrible counterparty risk and probable default. In the land of decentralized finance, where intermediaries don’t have to perform credit checks or comply with regulations, and where the value of your collateral goes up everyday, everything is supposedly possible (until it isn’t).

Yield farming in itself deserves a series of posts. To give you an idea of the stampede that it is, have a look at the volumes:

All this pile of crypto “value” is locked away in smart contracts, reducing supply and propping up prices. These smart contracts have varying levels of security, and not a week goes by without a new exploit being announced, and “yield farmers” losing tens of millions of funds to hackers. But because returns are so high, nobody cares for now.

USDT counterparty risk

USDTs look like real money to users because exchanges and arbitrageurs maintain a peg to the dollar - the price of every cryptocurrency is the same for USD as for USDT. However, USDTs come with a very important caveat: their apparent value relies exclusively on trust and hope that this peg will hold. There are no guarantees that USDT will be worth anything tomorrow - which is a pretty sweet deal for exchanges who keep the balances of their clients in USDT, instead of USD. If Tether collapses, it’s the users who will get shafted, not the exchanges.

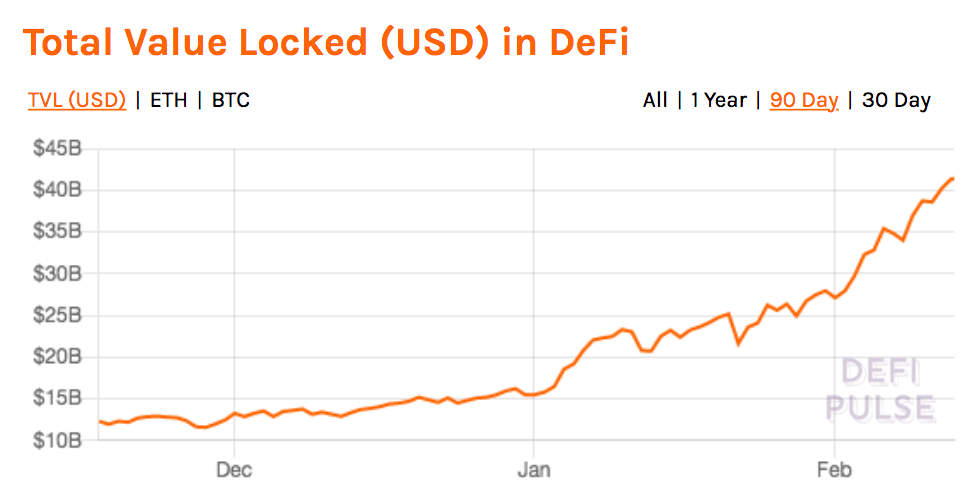

The use of USDT has thus divided the crypto ecosystem in two separate worlds: one “regulated”, the other - a crapshoot of YOLO gambling disguised as “investments”. A simplified view of this ecosystem:

Notice how PayPal and Robinhood have chosen to isolate themselves from the rest of the ecosystem, not allowing their users to withdraw their crypto? They know allowing outside transactions is a ticking time bomb, and they want no part in the blame game that will happen after the collapse.

Tether can collapse in two ways:

- regulatory action: the STABLE act, by requiring stablecoins to have proper backing and audits to the same level as money-market funds, would force Tether to cease its operations. As noted time and time again, it’s very unlikely that USDTs are properly backed. Other pieces of legislation, like the ones looking at AML & KYC would have even worse effects. Crypto exchanges, unlike banks, aren’t currently required to perform KYC and AML procedures on the destination account because they’re classified as simple money transmitters. Stablecoin issuers aren’t required to know the identity of individuals who are holding their stablecoins. When this changes, the crypto ecosystem will collapse.

- natural, albeit sudden, death: the crypto ecosystem is built on the assumption that prices can only go up. Yield farming requires prices to go up to pay out the astronomical returns it advertises, and that investors expect. DAI needs the value of its collateral not to go down, or it runs the risk of cascading liquidations, where the liquidation of one position brings down the value of the collateral for other positions, and leads to ever more liquidations. USDTs being most probably backed, directly or indirectly, by Bitcoin, if the price of Bitcoin goes down, insiders who hold USDTs will want out, creating their own cascade of liquidations and forcing Tether to close shop.

USDT collapse playbook

One USDT isn’t worth one dollar. It only appears so, because exchanges - both on-shore and offshore - have an economic interest to maintain the peg.

Because USDTs are used as collateral for leveraged trading, offshore exchanges need to maintain its value or risk a cascading liquidation event for the positions of their clients. Regulated exchanges have an interest to keep the prices of crypto quoted in USD in line with those quoted in USDT, because if the prices quoted in USDT are higher, everyone will understand that USDTs are worth less than USDs, and offshore exchanges will collapse. And because on-shore exchanges serve as on-ramp for offshore leveraged trading (and gambling), they have an interest in keeping the flow going. Moreover, as USDTs are used to pump Bitcoin up, onshore exchanges also benefit from the increased interest in crypto as people buy to HODL.

Because of this alignment of interest, USDT is able to set the pace for the whole ecosystem while only controlling a part of it - quite like the Willy Bot managed to pump up the price of Bitcoin everywhere, while only being active on MtGox.

However, the moment insiders realize USDT’s game of musical chairs is coming to an end, the two sides of the crypto ecosystem will turn from friend to foe in a second. Actors on the USDT side have little access to banking, and their only way of cashing out is to buy a liquid crypto currency (like Bitcoin), and transfer it to the regulated side, where it can be sold for real dollars, instead of a collapsing USDT. We’ve seen this pattern in 2013, when the price of Bitcoin on MtGox shot through the roof as people tried to buy it and transfer it to exchanges that weren’t bankrupt. Expect the same to happen again, with Bitcoin priced in USDT going to the moon, while Bitcoin priced in USD is crumbling.

When offshore players realize the gig is up, they will disappear with their customers’ crypto. Bitcoin won’t collapse to zero, because a large number of people won’t be allowed to cash out, their coins getting stolen. These coins will slowly get back on the market over the next few years, as a result of successful lawsuits (just like for MtGox), or as insiders who disappeared with their customers’ funds slowly come back out of hiding and try to cash out while keeping a low profile (just like for fraudulent ICOs).

Regulated exchanges will try to cut themselves off from the collapse. They’ll suddenly start to care a whole lot about KYC and AML. Coinbase won’t touch Bitcoin that’s been on Binance’s wallets with a ten foot pole. But regulators will come after them nonetheless, as the public outcry will be just too great. A lot of people will lose everything, and with crypto having gained an air of credibility with official, trusted outlets like Bloomberg, Reuters or CNBC covering it in a legitimate way, the outrage will be justified.

Rise, repeat

For the last 10 years, this cycle of pump and screw has set the pace for Bitcoin’s rise from $50-ish to almost $50k. Naïve investors are drawn into the game by the promise of incredible returns, fuelling a bull run. When the inflow of cash no longer allows for the scam of the moment to continue, one way or the other, those naïve investors get their coins taken from them, in exchange of MtGox IOUs, ICO shitcoins, or - in this cycle - worthless USDTs.

Because investors are never allowed to sell, Bitcoin doesn’t go to zero, its price hanging around aimlessly, until a new use case for Bitcoin’s pseudo-anonimity is found and a new serving of hapless suckers is sheered.

Caveat emptor.