Ripple the company’s existence evolves around denying that it has anything to do with Ripple the coin. It’s obvious that they are inextricably linked, first because they are both called “Ripple”, and then because Ripple the company owns the majority of Ripple coins. However, their whole business model is dependent on XRP, the Ripple coin, not being legally associated to the Ripple company. Here’s why.

Ripple’s Business Model: Selling Worthless XRP Coins To Clueless “Investors”

Ripple the company is unique in the sense that it doesn’t make money from selling its product. It makes money by selling its stash of XRP coins to naive “investors” (let’s call them “XRP bagholders” for more clarity). Ripple is very transparent about this - they even issue regular reports like this one, where they announce how many XRP coins they’ve dumped on XRP bagholders. In 2018 alone, Ripple has made over $500 million selling XRP coins.

XRP bagholders buy XRP coins because they believe that XRP coins are worth much, much more than what they’re selling for right now. The reason for that belief is that Ripple goes to great lengths to communicate on how its technology will change the world, and how it will be used by every financial institution for transfers and settlements - which is the core of banking.

The main argument for why XRP coins are worth something, is that Ripple’s technology will supposedly render obsolete the nostro/vostro account system, which supposedly requires $5 trillion to be frozen today. Because this pile of cash will be freed up, the reasoning goes, it will be somehow replaced by XRP coins, thus somehow giving XRP coins an equivalent market value of $5 trillion, or $50 per coin. This is all explained on Ripple’s own website.

Currently, XRP coins trade at around 30 cents, so the nostro/vostro argument induces hopes of 15,000% returns for XRP bagholders. Other Ripple-friendly sources have gone to great lengths to inflate this potential valuation, suggesting that one XRP coin could be even worth over $500.

None of Ripple’s So-Called Clients Actually Use Ripple’s Technology

In previous posts, I pointed out that most of Ripple’s so-called 200+ clients have of “financial institution” only the name, or that, like Santander, they just pretend to use Ripple’s technology.

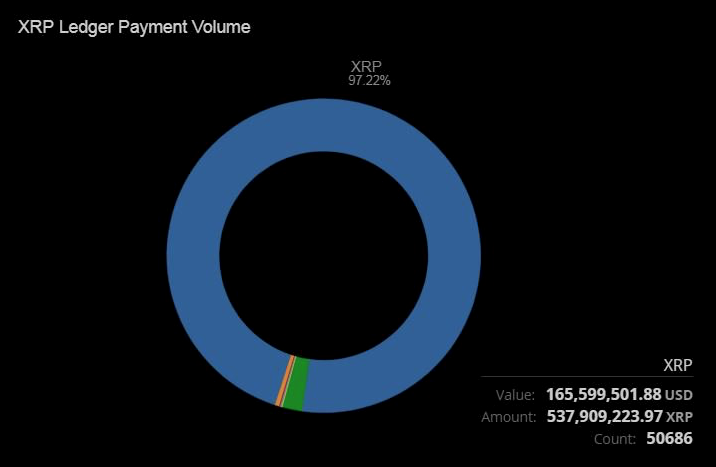

Colin Platt (@colingplatt) directed me to the following chart, coming from Ripple itself, which illustrates that only $2 million was transferred over a period of 24 hours using Ripple’s technology, and that virtually all the transfer volume, or 97,2%, was pointless XRP coin flow.

Ripple claims to have such amazing clients as Amex, Santander, Standard Chartered, Mitsubishi UFJ, MoneyGram, BBVA, etc.

How come all these financial giants put together only managed to generate a pathetic $2 million of transactions over 24 hours?

The relentless PR about partnerships being signed, and proof-of-concept projects being launched, is what Ripple is really about. It’s much, much easier to shill XRP coins and dump them on clueless XRP bagholders, than it is to come up with a real product and sell it to clients.

The Nostro / Vostro Argument Is Bullshit

The nostro - vostro argument is bullshit for three reasons.

Banks will never use Ripple’s tech at scale.

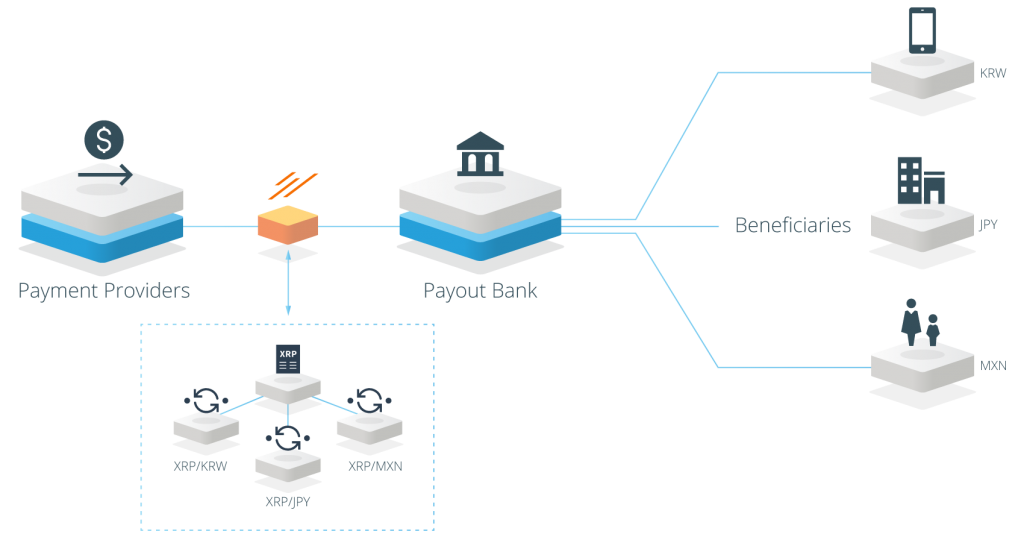

xRapid relies on banks buying virtual coins, sending them instead, and then hoping that someone will buy back the coins for real money. Ripple has come up with a nice infographic to illustrate this amazing process:

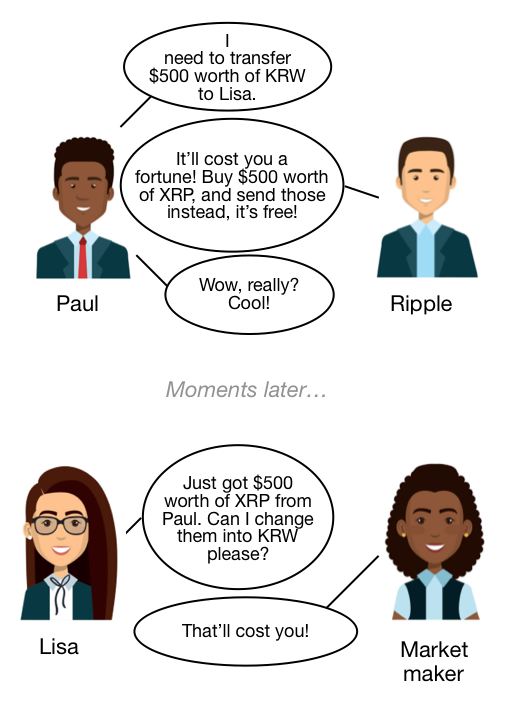

A much more realistic illustration would be:

The whole system relies on the existence of virtual coin / real money market makers with very deep pockets. And this market-making service will be very expensive.

If banks one day use Ripple’s tech, they won’t need that many coins.

If trillions are currently supposedly locked in nostro and vostro accounts, it’s because every bank needs to be sure to have enough funds in case a string of big transfer orders comes up, in all the bank it has nostro accounts.

With xRapid, all the banks taken together need only as many coins available as the biggest transfer order ever, because the order is executed instantly, and the coins become available in seconds for the next transfer order. Remember the $5 trillion figure? If transfers become instantaneous, the need for capital shrinks to a few billion, even less than the current market value of all XRP coins taken together.

If banks one day use Ripple’s tech, Ripple doesn’t have to use XRP coins.

This is one of the reasons Ripple (the company) doesn’t want to be associated to XRP (a.k.a. Ripple the coin). Ripple doesn’t want to be legally bound to make good on any promises they might have implied to XRP bagholders. In case of a miracle, if Ripple somehow manages to pull a flying pig out of its hat and xRapid (or any technology Ripple manages to come up with in the future) is indeed adopted, Ripple will be free to ditch XRP, issue a new coin in the blink of an eye, and use that coin instead.

This legal position is standard for so-called crypto companies. EOS, for example, states that:

The EOS Tokens do not have any rights, uses, purpose, attributes, functionalities or features, express or implied, including, without limitation, any uses, purpose, attributes, functionalities or features on the EOS Platform. Company does not guarantee and is not representing in any way to Buyer that the EOS Tokens have any rights, uses, purpose, attributes, functionalities or features.

block.one

As long as XRP coins aren’t associated to Ripple Labs, they are legally nothings. During UK Parliament hearings, Ripple representatives were very defensive about their connection to the XRP coin. Ryan Zagone, Ripple’s director of regulatory relations, stressed that

“XRP is open source and it was not created by our company, so that existed as an open source technology. We created a company that was interested in modernizing payments and then began using that open-source tech to do so … We didn’t create XRP … What we do have is we do own a significant amount of XRP, it was gifted to us by some of the open-source developers that created it. But there’s not a direct connection between Ripple the company and XRP.”

coindesk.com

XRP Bagholders Aren’t Entitled To Anything

Even if Ripple manages to one day come up with a technology that banks actually use, XRP bagholders won’t see a cent of the profits Ripple will make. It will all go to Ripple Labs shareholders, among which one can spot names like Standard Chartered and Santander. Surely the fact that these two banks are Ripple investors, had nothing to do with them both claiming to use Ripple’s technology.

XRP coins are, for all purposes, completely worthless. They only have a price above zero because people buy them, fooled by Ripple’s lies and deceit. The moment people stop buying XRP coins, Ripple Labs will disappear, because their business model will no longer make sense. But not before making billions in an obvious scam, that’s only possible because XRP bagholders lack the basic understanding of what’s a real financial security, and why those are worth something.

David Schwartz, Ripple’s CEO, admitted himself that Ripple’s goal was to do everything in its power to pump and dump XRPs onto clueless bagholders:

“After all, the reason we’re doing this is to increase demand for XRP to increase the value we can extract from our stash of XRP”.

David Schwartz, Ripple’s CTO

(Special thanks to @buzimovicz for the clue).

XRP shills didn’t talk much about that slip of the tongue, for some reason.

What a BS article. How do you dream up this verbal diarrhea?! The stench of this misinformation is quite intoxicating.

You farkin shill. Your research is flawed you idiot. Are you retarded?

These articles are awesome and hilarious. Please keep it up.

That quote by the CTO is a doozey. It seems like a matter of time before this house of cards collapses.

“In 2018 alone, Ripple has made over $500 million selling XRP coins.”

Right. So now what?

Ripple is buying yachts and private jets with that money? Or is there a chance they have better investment plans?

Ripple made it very clear that this is a marathon.

Actually, every IT project I know of is a marathon. Now, add to that the fact that financial businesses are traditional/conservative, or even that they just don’t want to change.

What do you get? A walk in the park? Nope.

One must start somewhere and then try, work, work harder, have some luck, then try again etc.

Do you remember how Microsoft began?

The question you have to ask yourself: are you content with how the financial world operates?

Do you think there are area’s which could/should approve?

Microsoft began by coming up with a product that people wanted and used, not by selling worthless magic beans to people claiming that one day these beans might be worth a lot of money, but not right now because they need more time.

You skip most part of my comment, then pick Microsoft to talk about. The one company I actually do know something about.

MS understood marketing like no other company. Not great software made them great. Trust me on this one. Grand-nannies stood in line, actually buying Windows95, while not having a PC. I am not kidding.

Anyway, what do you consider having value? That depends on many rational and irrational factors. Would you pay $10000 for a pair of used socks? How about from Elvis?

Thing is: 3 guys invented something. At that time didn’t even knew if it had value or not or what to do with it. They where techies.

They made something out of nothing and people believed in it. Are you sure they where only after the money?

Or could it be that cynicism took the better half of you already?

One fact still remains; Ripple wants to change something in finance.

You may dislike that, if you have a specific agenda you probably will.

Disclaimer: yes I hold XRP, but not blindly.

If XRP has no possible future what cryptos do?

Why so obsessed with Ripple and XRP? people don´t listen to you anyway. You´re just a troll:)

Xtremely Retarted People Army we need more hillarious abusive comments. Please kind sir, for the sake of comedy.