After the release of JP Morgan’s JPM Coin, Brad Garlinghouse, Ripple Labs’ CEO, was quick to criticise the new cryptocurrency for being closed-ended and for JP Morgan’s internal use only. Ripple Labs, on the contrary, prides itself in having established an open standard, with a network of users they call “RippleNet”. In reality, RippleNet is everything but a network, and will never be, because Ripple Labs doesn’t understand KYC and AML requirements.

The crypto community has welcomed the news of JP Morgan issuing its own cryptocurrency (the JPM Coin), intended to facilitate transfers, as a sign that Ripple Labs was up to some serious competition. Indeed, JP Morgan, with all its know-how, resources, brand power, and existing partnerships, seems to be in a much better position to introduce a solution for global payments, than a smallish Silicon Valley startup with close to no experience in banking.

Brad Garlinghouse, Ripple Labs’ CEO, was quick to dismiss the threat as irrelevant, on Twitter:

As predicted, banks are changing their tune on crypto. But this JPM project misses the point – introducing a closed network today is like launching AOL after Netscape’s IPO. 2 years later, and bank coins still aren’t the answer https://t.co/39EAiSJwAz https://t.co/e7t7iz7h21

— Brad Garlinghouse (@bgarlinghouse) February 14, 2019

Mr Garlinghouse’s tweet linked to a LinkedIn post from 2016 that was meant to reassure XRP investors about Ripple still being on top of things, and included this very bizarre statement:

“The second big problem with the ‘utility settlement coin’ is it seems it’ll be backed by a basket of currencies. Once backed by cash, it’s no longer an asset; it’s a liability.”

Brad Garlinghouse, CEO of Ripple Labs

It seems strange that the CEO of a company whose stated goal is to disrupt banking, doesn’t understand double-entry accounting, and the notion that one man’s liability is another man’s asset.

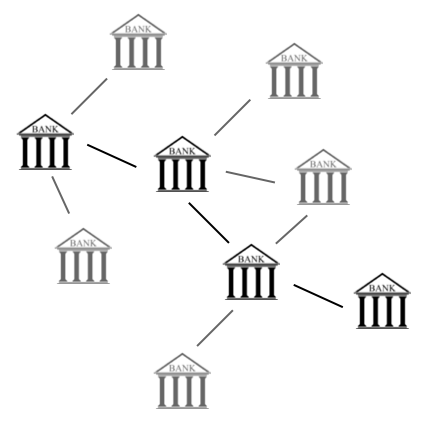

The supposedly amazing RippleNet network

The point that Mr Garlinghouse was probably trying to make, was that only a coin independent from any single bank, could ever be used as a global means of transferring value. A coin like XRP for instance, taking cue from Ripple’s own website:

“RippleNet customers can use XRP for on-demand liquidity while still ensuring payments are sent and received in local currency on either side of a transaction.”

ripple.com

The website doubles down:

“RippleNet makes it easy to connect and transact across its robust network of 200+ banks and payment providers worldwide.”

ripple.com

Mr Garlinghouse poked at JP Morgan’s “closed network” model as outdated, as opposed to RippleNet, an “open network” where everyone can supposedly transact with everyone else.

Except that this is, of course, a lie. RippleNet is no network - it’s just an alphabet soup of so-called partners, most of whom don’t transact with anyone else.

Ripple doesn’t understand KYC and AML

With over 200 so-called “customers”, Ripple is yet to provide an example of banks who have used Ripple’s technology to transact in a smooth, multilateral way, without already knowing each other, like in a real network. It’s most famous customers: Santander, BBVA, SBI, all have used Ripple Labs’ solutions only to transact with themselves, or a very limited number of banks they already knew:

- Santander has released a mobile app, One Pay FX, that lets Santander’s customers make transactions with other Santander’s customers in four countries

- BBVA has made one live test of transferring money from BBVA Spain to BBVA Mexico

- SBI Ripple Asia has released a mobile app, Money Tap, that lets customers of SBI Sumishin Net Bank, Suruga Bank and Resona Bank make transactions among themselves.

The reason why banks only use Ripple’s technology to transact with themselves and very close partners, is because Ripple doesn’t solve the real bottleneck for cross-border transactions: KYC (Know Your Client) and AML (Anti-Money Laundering) requirements.

To understand why this is a problem, imagine that Joe wants to send $100 from its account at Santander to Jane, whose account is at Société Générale.

Société Générale has to check who is Joe (KYC) and why is Jane receiving the $100 (AML). And it can be complicated - Société Générale doesn’t know Joe, and Santander doesn’t necessarily have all the exact documents that Société Générale might need, as the two banks operate in different jurisdictions, and have two separate systems for keeping records. It all takes time and money to sort out.

The fact that partners within RippleNet can’t transact with each other is hardly news. When Ripple went to see SWIFT to demonstrate their fancy database, back in 2015, SWIFT had this to say:

“You may have an open technology framework but if those control mechanisms are not there, banks will not adopt that because they can’t. That’s why we have relationship management features in the Swift network.”

Wim Raymaekers, global head of banking markets at Swift

Ripple’s claim of solving cross-border transactions is a joke

Currently, banks transact using the so-called corresponding banking model, where every bank in the world has a limited number of relationships with other banks, where it has agreed on common standards of communication. If a bank doesn’t have a direct relationship with a bank he needs to send money to, it will try do find a path through its relationship network.

Ripple claims that by using its technology, banks will be able to transact directly without intermediaries. However, without a common standard for documenting clients and the origin of their funds, that’s just impossible. And that’s out of Ripple’s, or anyone’s, control: banks all over the world have different rules and standards for record-keeping, due to varying requirements by jurisdiction, and heterogeneous internal processes.

To claim that banks could use its technology to transact directly all over the world, without knowing one another, would require Ripple to be completely ignorant of banking regulations. Which, given Mr Garlinghouse’s bizarre LinkedIn post, is more probable than not.

KYC & AML is the reason why banks only use Ripple’s technology to transact within their own boundaries, or with a few other banks they already know - exactly like with the current correspondent banking system.

If you dig a little bit deeper into Ripple’s uber-positive press releases, you’ll see that every single one of Ripple’s so-called customers is using Ripple in a very limited way, either within its own boundaries, or only with a few banks it already has a relationship with:

“MercuryFX will be testing payments into Mexico & Philippines with Ripple.”

https://www.mercury-fx.com/market-news/announcements

“Further leveraging the partnership with Ripple, RAKBANK’s RAKMoneyTransfer (RMT) services enables customers to make instant, frictionless, and secure money transfer services to Sri Lanka’s Cargills Bank via blockchain using Ripple platform.”

https://static.mubasher.info/File.Mix_Announcement_File/44681B59-6D6B-4A1D-8EF8-E1E22CB82A44.pdf

“Siam Commercial Bank (SCB), in collaboration with Japan’s SBI Remit, is using Ripple’s blockchain enterprise solution to power real-time remittance payments between Japan and Thailand.”

https://disruptive.asia/scb-sbi-ripple-blockchain/

But, but, but, using Ripple for transactions is so much cheaper for banks, right? Of course it is, because Ripple pays them.

Ripple doesn’t solve anything. It only pretends it does, so that investors keep buying its XRP coins. But with JP Morning releasing a direct competitor to XRP, Ripple’s business venture might come to an abrupt end.

Concise, thank you

Stupid maximalist thinking. Thank you.

XRPChat community is afraid of JPM coin. If you bring it up they just reply “fud!!!” and then ban the guy who posted the link, and delete the thread.