Ripple claims that banks will use its technology to perform fast cross-border transfers. When that comes, they will need to buy XRP coins, and that’s why XRP coins are valuable. In reality, Ripple doesn’t stand a chance, and it must know it. It’s argument that XRP coins are worth anything at all, is a flat-out lie.

In 2018 alone, Ripple Labs sold over $500 millions’ worth of XRP coins, mostly to unsophisticated investors. Ripple’s only argument for why XRP coins are worth anything at all, is that banks have to buy them if they want to transact using Ripple’s technology:

The point of XRP, at least as far as Ripple’s use case is concerned, is to settle institutional payments using an open digital asset with liquidity that anyone can contribute to and draw off of. It’s to put banks on the same playing field as non-banks.

— David Schwartz (@JoelKatz) September 3, 2018

Ripple claims that banks are quickly adopting its technology, and that it is on pace of competing with SWIFT for a share of the global cross-border transactions market. As a result, XRP coins’ market capitalisation should supposedly rise to a sizeable fraction of the $5 trillions the nostro / vostro system currently requires.

The origin story

The first time Ripple Labs mentioned the nostro / vostro use case for XRP, was in a letter to the HM Treasury, dated 3 December 2014. It was one in a list of five use cases for XRP, where “Small and Mid-Sized Banks can benefit by having direct access to international payments without tying up large amounts of capital.”

Ripple went on to explore this use case by pitching its idea to banks over the course of 2015. It was floating the idea of a system where market makers…

“would credit their accounts in one country and debit them where the cash is to be transferred to, with Ripple’s distributed ledger recording the transfer of money between different countries.”

Dilip Dao, Ripple Labs Asia Pacific CEO, 2015

Ripple also went to see SWIFT, the company with a monopoly on interbank messaging, to try and see what they thought of their technology. SWIFT tested Ripple’s technology back in 2015, and were unimpressed:

“You still need business rules on top of that and you still need the payment information anyway. That’s not in a distributed ledger technology, at least not today.”

Wim Raymaekers, global head of banking markets at Swift, 2015

Ripple’s idea was dead in the water

At the time, SWIFT was already working on its own solution to improve on cross-border settlements, and accepted to run a test with Ripple to see if there was something there. They didn’t think it could be used for settlements or payments. The biggest bottleneck in inter-bank transfers is the need to comply with KYC and AML requirements.

“[Blockchain is] a great technology but you still must know who you are transacting with. So there must be identity, there must be some kind of organisation around this.”

Wim Raymaekers, global head of banking markets at Swift, 2015

SWIFT’s solution was already solving for KYC & AML, with a global registry of banks that were using SWIFT. At the time when Ripple was just trying to figure out what cross-border settlements were all about, SWIFT was already lightyears ahead:

“We now have over 1,000 banks. It’s aimed at correspondent banking. It’s ‘know your correspondent bank’ rather than ‘know your customer.'”

Gottfried Leibbrandt, chief executive of the Belgium-based SWIFT, 2015

Ripple chose to double-down on its bluff

In 2016, McKinsey published a report about the state of global payments, which outlined the efforts that banks were making in order to bring down transaction costs. If you did a little bit of research about Ripple, you must have come across that report, because Ripple links to it from its “Liquidity Explained” page:

This report is the cornerstone of Ripple’s business plan. Ripple references the report as the source for saying that $5 trillion are currently trapped in nostro / vostro accounts, and that Ripple’s technology will free up all this capital, replacing it with XRP coins.

Without this argument, there’s no way Ripple could make a case for why people should buy the XRP coins it has given itself, and is currently selling to unsophisticated investors. Ripple Labs’ would lose its sole source of revenue, and the hundreds of millions of dollars that come from it.

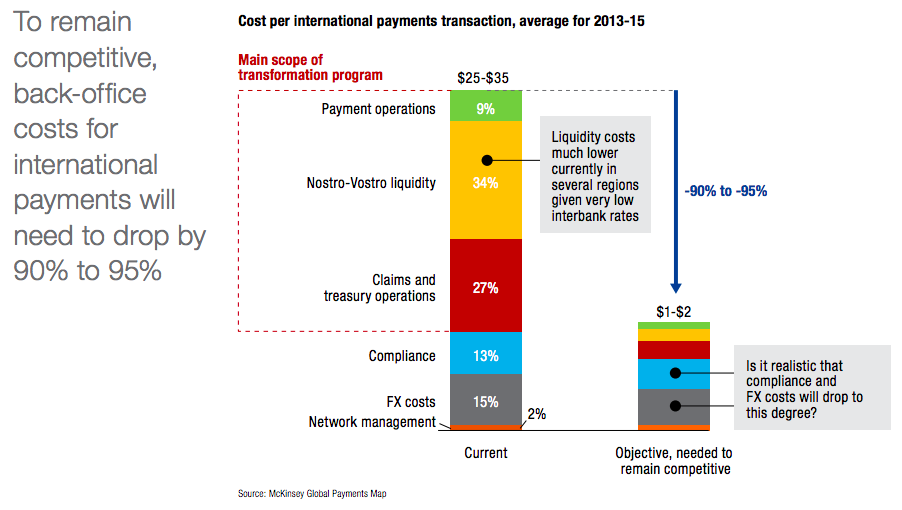

The problem is, the McKinsey report Ripple links to, doesn’t say anything like what Ripple pretends it does. It doesn’t even put a number on the amount of capital supposedly trapped in nostro / vostro accounts. On the contrary, the report projects that efforts being done by banks will bring the average cost of a cross-border transaction down to $1-2, effectively destroying Ripple’s whole argument for why banks should need its technology at all:

SWIFT gpi is beating Ripple to a pulp

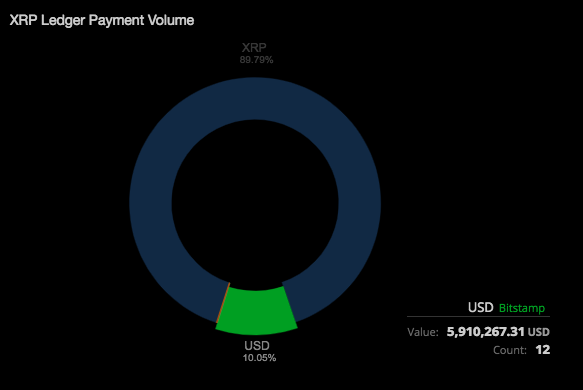

Ripple keeps claiming that it will disrupt SWIFT, but SWIFT is already disrupting itself, leaving Ripple in the dust. As I’m writing this, by Ripple’s own account, its ledger was used to transfer $10 million over the last 24 hours:

SWIFT’s own solution - SWIFT gpi, the one they already had been working on for years when Ripple came along, is currently doing $300 billion transactions per day, with over 400 financial institutions actively using it.

Anyone with a modicum of understanding of international banking already knew back in 2016 that Ripple didn’t stand a chance to disrupt anything. SWIFT’s Wim Raymakers was already pointing out that Ripple’s amateurish partnerships with banks were worthless, and a joke:

“The gpi is different from some proof of concepts out there. You know, where they (Ripple) say we sent a payment in 3.5 seconds from bank A to bank B; that is typically a demo; there are no real bank back-office systems behind it.”

“So here we took the complete opposite approach. Banks are actually coding this gpi into their systems; they are automating the gpi flows. That’s what they are testing now in pilot on their production systems.”

Wim Raymaekers, SWIFT’s global head of the banking market, 2016

Ripple is defrauding XRP investors

Ripple was never even close to being adopted by banks for its supposed merits, because it has none. The real problem that needed to be solved in cross-border transactions was KYC & AML, not writing numbers in a database. It’s a much more complicated problem, which SWIFT was already working hard at solving. Ripple didn’t even try to compete with SWIFT. Instead, it simply put out empty press releases about how distributed ledger technology will solve everything, and hopped onto the blockchain train, at the expense of XRP investors.

Ripple’s continuous press releases about how its technology is supposedly being adopted by financial institutions, have but one goal: to induce unsophisticated investors into buying the XRP coins it’s continuously selling.

Great post, well researched. The XRPChat community will have no response to this; they ban users who link to your site.

Well researched. Lol. People pick this apart without trying. You would too if you researched XRP. He is a Ripple hater. So just trying FUDing. I would imagine he is eye balls up to debt in bitcoin and slowly realising bit coin is just gonna be a collectors item and not used on a worldwide scale.

Think about this: why SWIFT developed GPI ? Because there is a competitor and they know what Ripple can do to their business. You clearly don’t see the whole picture, with Ripple relationship with IMF, World Bank, Bilderberg Group and so on. Keep going with your articles, this way you’re doing some research and in a matter of months you’ll go from a non-believer into an XRP investor.

“Bilderberg Group and XRP” into google… oh wow. God help retail investors.

*standingovation.gif*

lol the kool-aid is strong!

SWIFT is owned by banks and run for banks. Why would they ever replace it with a privately held corporation/asset? Banks will never buy XRP except at a steep discount from Ripple to offload on naive retail investors.

You either believe that decentralized digital assets running on a software platform build from scratch over the last 6 years, will power the global fully automated real time Internet economy, or you think the old tech built 30-50 years ago is not a spaghetti mess in which correspondent banks have positioned themselves as rentseekers like bugs, works fine, just needs to spin the rentseeking process faster.

The innovation of a decentralized digital asset is that the value is entirely encapsulated in digital data, does not rely on anything other than cryptography and online available data, can be verified programmatically, does not have a counter party and the transactions do not have any intermediary. That is what makes this type of asset transferable as easy as data, and this is the missing component of the Internet. Cross border payments is just one usecase, paying for content and online services, and getting paid for content and online services is a vastly bigger one.

And let’s not forget nearly half of our population that does not have a bank account (so no relation with any swift partner), but mostly do carry a mobile supercomputer in their pocket, ready to install any app that solves the global payment problem, so they also can join the global online work- and entertainment force, the potential of which has yet to be unlocked.

So again, you either believe in the true innovation that digital assets bring to the Internet, or you don’t. If you do, XRP clearly has the best technical characteristics for payments, is designed to become the most decentralized, with the highest throughput, and with the smallest carbon footprint.

So, in addition to competing (and losing) to SWIFT’s GPI - XRP is positioned to lose, not only to Venmo and the Cash App as an MoE (as USD is less volatile as, and is only intended for transactions) but it is also being choked by bitcoin and the Lightning Network as a viable SoV/ DLT-protocol, because of a lack of A) international and B) local interest. Also, almost no platform support exists for XRP from the most popular (US native) crypto companies (Gemini, Coinbase, Square, and eventually Twitter?) as the smartest, brightest, and most entrenched tech entrepreneurs recognize dodgy p.o.s flame heaps when they see them, and have avoided XRP affiliation at all costs in order to preserve reputation. Hollywood idiots have successfully been brought into the XRP scam, however this is not worth noting, as reputations as ‘artist’ are robust and difficult to be sabotaged.

All claims without fundamental reason why plus the wrong number lead me to wonder the purpose of the post

” Ripple Labs’ would lose its sole source of revenue, and the hundreds of millions of dollars that come from it.” — Are you sure XRP is Ripple’s only source of revenue? I though they also make money from licensing and installing Ripplenet. If you could compare the two, it’d be great.

There’s no way of knowing exactly. Only Ripple’s management could provide that information, but I doubt they ever will.

There’s a few tidbits out there, some seems contradictory:

David Schwartz, May 25 2017 -

“Ripple holds a huge pile of XRP and will be the dominant XRP holder for the foreseeable future. But we’re primarily VC financed and we get revenue from selling software to banks. We don’t use our XRP as a bank account but as a strategic weapon. (Though we do sell some for revenue, we just don’t need to for salaries or to keep the lights on.)”

Garlinghouse, Oct 23 2017 -

“Suffice to say we’re cash flow positive and that give us the ability to invest in a way that’s good for the eco-sytem and our company. Absolutely, we harvest some of the XRP. It’s very important for us to be very transparent in XRP markets so every quarter we publish a report that specifies how much we sold in the open market and to institutional buyers.

No, we wouldn’t be cash-flow positive without the XRP sales. It goes back to the fact XRP is a strategic weapon to invest in the ecosystem. It gives us flexibility to hire the best engineers in the world and to invest in the platform and the technology.”

In between, they probably got to the point where XRP market was deep enough for them to start selling their stash of coins, and to get revenue this way.

Guys, just see the facts. XRP needs seconds to settle (3-6 secs). Billions are settled in secs. See some of transactions done on XRP ledger. XRP is the settlement tool. SWIFT is messaging tool. XRP can settle literally anything, currency, stocks, bonds, etc. in seconds not in days. Swift needs more than T+1 days to settle. Ask any bank or payment provider which has adopted its technology. Check for yourself.

Sure, have YOU checked?

SWIFT doesn’t need days to settle. SWIFT gpi, which is SWIFT’s new solution that came out in 2016, settles half the transactions in less than 30 minutes. It’s currently processing $300 billion worth of transactions per day. Ripple’s pretend solution has been around for much longer, but barely manages to reach $10 million per day. Ripple’s network processes 30,000 times less than SWIFT gpi, a tool that came out after Ripple. Maybe there’s a reason.

Banks can settle in seconds too. Nanoseconds even. That’s how databases work!

It’s KYC/AML that takes T+1.